Here's why taking a mortgage holiday isn't the end of the world

If we see one more bug-eyed commentator on TV terrifying homeowners over the perils and pitfalls of mortgage holidays, I might have to bust out of lockdown and hunt them down.

If there's another column-inch labelling the strategy a "holiday from hell" or a "last resort" the morning newspaper may spontaneously burn.

My inner frustration crystalised last week after seeing the psychologist Nigel Latta interviewed. The media flapped on behalf of parents and Nigel looked down the barrel of the camera and admitted it didn't matter one jot if they did no schoolwork. Gasp. He shouldn't say that. Yet he wasn't intending to be contrarian. There was a desperate need to convey perspective and reassure.

On that basis, let's give mortgage holidays a good Nigel-ing.

For those facing job-loss, taking a mortgage holiday is likely to be an absolute necessity. We are in a period of unprecedented and widespread financial stress on families. You should be reassured it's the best advice for the vast majority of people in this situation. Interest continues to be added to your mortgage at historically cheap levels, making payment deferral one of the most sensible financial strategies you could use right now. It is highly unlikely to impoverish you and won't matter a jot when buried amongst a lifetime of change.

Does that sound strangely positive and bereft of risk-warnings and doom?

Let me go out on an even bigger limb. Right now, you should consider using mortgage relief before using your savings to pay the bank. Why? With no emergency funds small financial hiccups can tip you over the edge emotionally. Being a sane and calm job-seeker who can cope with the small stuff, because the big stuff is taking a break, makes more sense. Yes, there are alternatives to mortgage holidays, such as interest-only, or tinkering with fixed rates and adjusting the terms.

There are only three levers a bank can pull and these only suit people who have taken a pay cut or have another good income in the family. For someone facing job loss, tinkering wont cut it.

How much does that break cost?

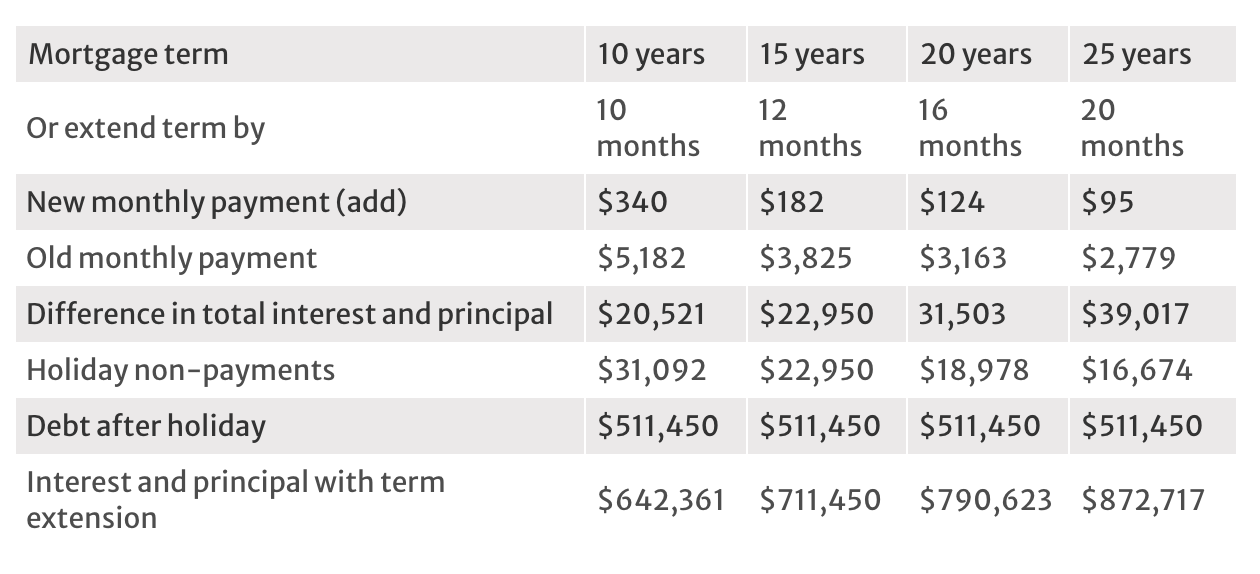

Mortgage Holiday: Six months on a $500,000 loan at 4.5%

When expertise fails us

The experts sometimes forget to be experts. They're trained to issue factual warnings and treat any negative financial decision with huge gravity, regardless of the environment it occurs in.

By getting involved in the flapping their confidence and power of reassurance becomes lost.

There are times when it's right to change the script you've been taught for a lifetime. Script-bias causes a mortgage commentator to fall over their feet with breathless warnings about interest payments compounding on your loan. Yet this is one of the most powerful tools for getting people back on their feet, maintaining calm and shoring up the property market.

If there was ever a time in history to blow the trumpet of a mortgage holiday, the day has come.

Let's reposition our thinking to help us cope:

My loan size will rise: So what? Just like capital gains, these are amounts on paper. House prices have been bounding up for years widening your equity gap. If both those values now get squeezed, it's just a blip on a long-term horizon. We are talking about adding half of 4.5 per cent if you're on a floating rate.

In the last three or four years alone you could have made 30 per cent gains. While some of this will disappear, most people have room to move in that gap.

The term of my mortgage will need to be extended: Indeed it will, but consider this. Life is not a straight line and our money doesn't exist in a vacuum. Over the coming decades you are going to get back on your feet. There will be pay rises, wage inflation, house inflation, inheritances, kids becoming independent and a savvy fixed rate to lock in. These all allow payments to be sped up. In the grand scheme of life you will never be able to accurately pinpoint this moment amongst the swings and roundabouts.

The average long-term interest rate has more impact. We can focus on the pain of accumulating interest for six months, but a small difference in rates over the life of a loan has far greater impact. For a $500,000 mortgage over 25-years, a one per cent difference has a saving of over $80,000. Your financial future is more in the hands of market conditions and your ability to negotiate deals.

Over payment: Interest rates have been falling, but when was the last time you reduced your mortgage payments? If you haven't, then you've been reducing the term. Chances are you're well ahead of the game. Beware of the numbers: Find the cost by comparing total interest and principal payments over the life of the loan, allowing for the accumulated interest. A mortgage of $500,000 over 25 years will grow to $511,450 after six months at floating rates. If you keep your monthly payment of $2779 the same when you re-start, it will add 20 months to the term.

But the first six months of this extension is offset by your payment holiday.

Janine Starks is a financial commentator with expertise in banking, personal finance and funds management. Opinions in this column represent her personal views. They are general in nature and are not a recommendation, opinion or guidance to any individuals in relation to acquiring or disposing of a financial product. Readers should not rely on these opinions and should always seek specific independent financial advice appropriate to their own individual circumstances.